What Is U.S. GAAP?

Explained from Scratch

A complete beginner-friendly guide to Generally Accepted Accounting Principles. From what GAAP actually is, to the 10 core principles, four financial statements, GAAP versus IFRS, and why these rules matter to every investor, student, and business owner in America.

Imagine two businesses selling the same product, making the same amount of money, but their financial reports look completely different because each one measures and records things in their own way. Without a shared rulebook, investors would have no way to compare companies, spot fraud, or make informed decisions. GAAP is that shared rulebook, and understanding it is one of the most useful financial skills you can develop.

U.S. GAAP, short for Generally Accepted Accounting Principles, is the set of rules and guidelines that companies in the United States follow when preparing their financial reports. It is not one single law written by Congress. It is a carefully developed framework built over decades by accounting professionals, regulators, and standards-setting bodies to make financial information consistent, honest, and comparable across the entire economy.

Whether you are a student taking your first accounting class, an investor reading a company's annual report, a small business owner trying to understand your own books, or simply a curious person who wants to make sense of the financial world, this guide will give you everything you need to understand GAAP from the ground up.

- 01 What Is GAAP? A Beginner Explanation

- 02 A Brief History of GAAP

- 03 Who Makes and Enforces GAAP?

- 04 The Three Key Objectives of GAAP

- 05 The 10 Core GAAP Principles Explained Simply

- 06 The Four Required Financial Statements

- 07 GAAP vs. IFRS: The Global Difference

- 08 Who Must Follow GAAP?

- 09 GAAP Updates and Trends in 2026

- 10 Frequently Asked Questions

📚 What Is GAAP? A Beginner Explanation

The full name says it all: Generally Accepted Accounting Principles. These are the rules that govern how American companies track, record, and report their financial activities. When a company publishes its financial statements, those documents are prepared according to GAAP. When an auditor signs off on a company's books, they are confirming that everything inside was done in line with GAAP.

Think of GAAP like the rules of a board game. Every player at the table follows the same rules, uses the same scoring system, and interprets the same cards in the same way. If each player made up their own rules, the game would be chaos. You could not tell who was actually winning. GAAP does the same thing for financial reporting. It creates a shared language so that when Apple reports a profit and when a small manufacturing company reports a profit, both numbers mean the same thing and can be compared fairly.

The word "generally accepted" is important. These are not random suggestions. They are officially recognized standards that the accounting profession, the U.S. government, and financial regulators have agreed to uphold. Breaking them is not just unprofessional. For publicly traded companies, it is illegal.

GAAP is the standardized set of accounting rules, requirements, and practices that companies in the United States must follow when preparing and presenting their financial statements. Its purpose is simple: to make financial information honest, consistent, and comparable across every company that reports it.

🕐 A Brief History of GAAP

GAAP did not appear overnight. It grew out of a series of financial crises and scandals that revealed just how dangerous unregulated financial reporting could be. Understanding its history helps you appreciate why these rules exist and why they matter so much today.

The Stock Market Crash and the Wake-Up Call

The Great Depression revealed that many companies had been reporting misleading financial information with no consistent standards to prevent it. Investors lost billions because they had no reliable way to evaluate what they were buying.

The Securities Acts and the SEC

The U.S. government created the Securities and Exchange Commission (SEC) and required all publicly traded companies to follow standardized accounting practices. The era of anything-goes financial reporting was over.

The Committee on Accounting Procedure

The American Institute of Accountants (now the AICPA) formed its first formal body to develop accounting rules. Over the next two decades it issued 51 official bulletins that formed the earliest foundation of what would become GAAP.

FASB Takes Over

The Financial Accounting Standards Board (FASB) was established as the independent, private-sector body responsible for developing GAAP. It replaced earlier committees and brought greater independence, rigor, and public representation to the standards-setting process.

The FASB Accounting Standards Codification

FASB launched the Accounting Standards Codification, reorganizing decades of standards into a single, searchable, authoritative source. This made GAAP dramatically more accessible to accountants, auditors, and educators. It remains the single official source of U.S. GAAP today.

The Convergence Project and Beyond

FASB and the International Accounting Standards Board (IASB) began a long project to harmonize GAAP with International Financial Reporting Standards (IFRS). While full convergence was never achieved, significant alignment occurred in areas like revenue recognition (ASC 606) and lease accounting (ASC 842).

🏛 Who Makes and Enforces GAAP?

GAAP is not made or enforced by a single organization. It is a system of layered authority involving a private-sector standards setter, a government regulator, and professional bodies. Understanding who does what helps you understand how financial reporting rules actually work in practice.

The Financial Accounting Standards Board (FASB)

FASB is the primary body responsible for developing and updating U.S. GAAP for nongovernmental entities. It is a private, independent organization, not a government agency. It was founded in 1973 and is funded largely by fees collected from public companies. FASB has seven full-time board members who serve fixed terms, and all of their deliberations, votes, and reasoning are made available to the public.

When accounting rules need to change because of new business models, new financial instruments, or shifts in how the economy works, FASB opens a public consultation process, gathers feedback from companies, investors, auditors, and academics, and then issues an update to the Codification called an Accounting Standards Update, or ASU.

State and local governments follow different rules set by a separate body called the Governmental Accounting Standards Board (GASB), also established in 1984. Federal government accounting is handled by the Federal Accounting Standards Advisory Board (FASAB). This guide focuses on FASB and the GAAP that applies to private and publicly traded companies.

The Securities and Exchange Commission (SEC)

While FASB writes the rules, the SEC is the government body that enforces them for publicly traded companies. Under the Securities Acts of 1933 and 1934, the SEC has the legal authority to establish accounting standards for companies listed on U.S. stock exchanges. In practice, the SEC has largely delegated that technical work to FASB, but it retains ultimate authority and regularly issues guidance, enforcement actions, and interpretations that influence how GAAP is applied.

When a publicly traded company files its financial statements with the SEC — which it must do quarterly (Form 10-Q) and annually (Form 10-K) — those statements must comply with GAAP. Intentional violations of GAAP in SEC filings can lead to massive fines, delisting from stock exchanges, and criminal prosecution.

The FASB Accounting Standards Codification

The FASB Accounting Standards Codification, launched in 2009, is the single authoritative source of U.S. GAAP for all nongovernmental entities. Before 2009, GAAP was scattered across thousands of separate documents, bulletins, and interpretations dating back decades. The Codification reorganized everything into one logical, searchable structure organized by topic. If a standard is not in the Codification, it is not authoritative GAAP.

🎯 The Three Key Objectives of GAAP

Everything in GAAP serves three fundamental goals. These are not abstract ideals. They have direct, practical consequences for how financial information gets used in the real world.

Illustrative representation based on financial reporting literature. Not derived from a single empirical study.

Consistency

Companies use the same accounting methods from one year to the next, so stakeholders can track performance over time without worrying that a change in methodology is disguising a change in actual results.

Comparability

Investors can accurately compare the financial health of Microsoft with Apple, or a startup with an established competitor, because both use the same accounting language and the same measurement rules.

Transparency

Standardized disclosures give investors, creditors, and the public enough information to make informed decisions. The rules reduce the risk of companies hiding important facts in the footnotes or using creative accounting to mislead stakeholders.

🔢 The 10 Core GAAP Principles Explained Simply

GAAP is built on a set of foundational principles that guide every accounting decision. These principles answer the big questions: when do we record revenue? how do we value assets? what must we disclose? Here are all ten explained in plain language with real-world examples.

Principle of Regularity

Accountants follow all official GAAP rules without exception. There is no picking and choosing which rules to follow. If it is in the Codification, it applies.

Principle of Consistency

A company applies the same accounting methods from period to period. If it switches methods (say, from one inventory approach to another) it must fully disclose the change and explain its financial impact.

Principle of Sincerity

Accountants provide an honest and accurate picture of the company's financial condition. The goal is truth, not flattery. A company that is struggling financially must report that struggle clearly.

Principle of the Permanence of Methods

The financial measurement procedures used in one period stay consistent over time. This prevents companies from selectively changing methods when the results would make their performance look better.

Principle of Non-Compensation

Companies must report all positives and negatives separately. You cannot net a liability against an asset or offset a loss against a gain just to make the numbers look cleaner.

Principle of Prudence

When there is doubt about a financial outcome, the more conservative estimate is used. This means recognizing potential losses as soon as they are likely, but only recording gains when they are actually realized.

Principle of Continuity

Also called the "going concern" assumption. Accounting assumes the company will continue operating into the foreseeable future. If that assumption is in doubt, it must be disclosed prominently in the financial statements.

Principle of Periodicity

Financial activity is reported in standardized time periods, typically quarters and years. This allows stakeholders to track performance over time and compare the same periods across different years.

Principle of Materiality

All information that could significantly influence an investor's decision must be disclosed. Small, immaterial items may be approximated. But anything that matters to a reasonable investor must be reported accurately and in full.

Principle of Utmost Good Faith

All parties involved in financial reporting are expected to act honestly and transparently. This applies to the company's management, its accountants, and its auditors. Deliberate misrepresentation is both an ethical violation and a legal crime.

Financial statements prepared in accordance with GAAP provide information that is useful to present and potential investors, creditors, and other users in making rational investment, credit, and similar decisions.

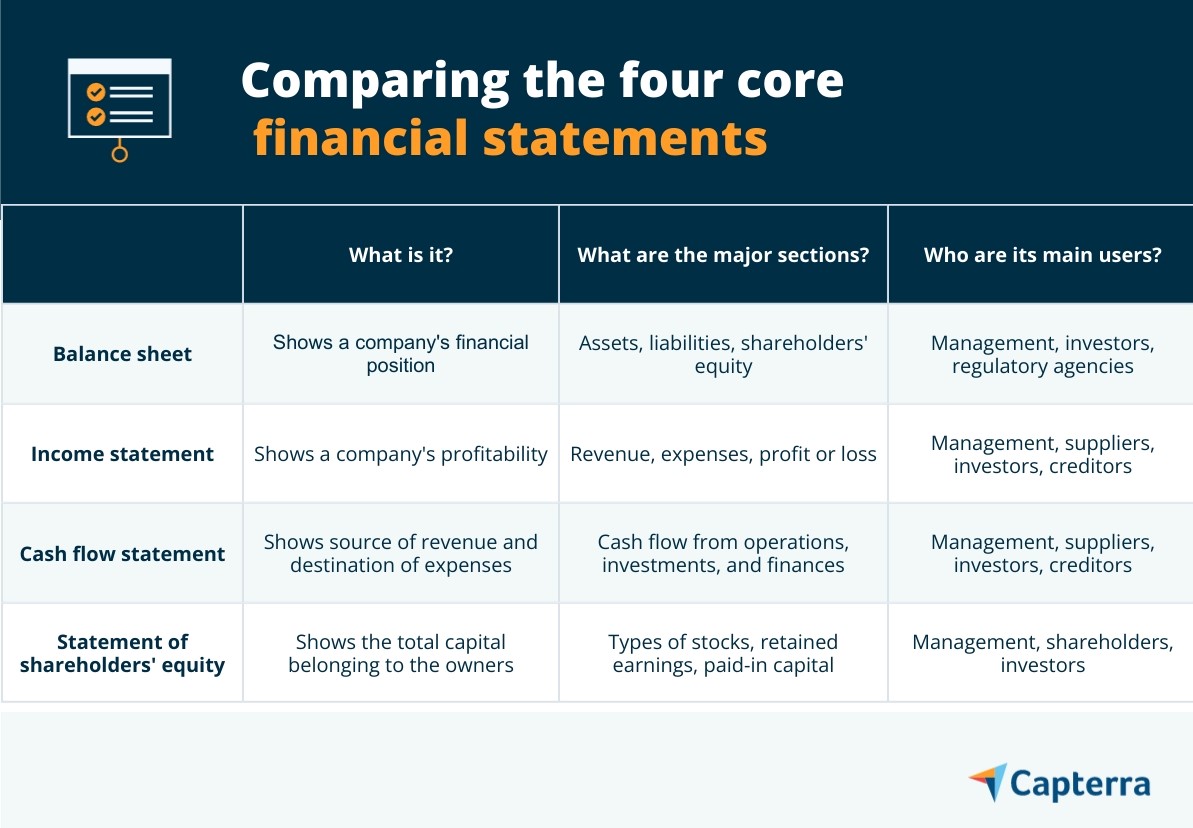

FASB Concepts Statement No. 1 · Read at FASB.org📄 The Four Required Financial Statements

Under GAAP, every company that follows these standards is required to produce four specific financial statements. Together, these four documents give a complete picture of a company's financial health. Think of them as four different windows into the same building. Each one shows you a different angle of the same truth.

The Balance Sheet

The balance sheet shows what a company owns, owes, and is worth at a specific moment in time. Think of it as a financial photograph taken on the last day of the reporting period.

It is built on the fundamental accounting equation: Assets equal Liabilities plus Shareholders Equity. This equation must always balance perfectly, which is why the statement gets its name.

- Assets: Everything the company owns or controls that has value (cash, buildings, equipment, inventory, receivables)

- Liabilities: Everything the company owes to others (loans, accounts payable, deferred revenue, bonds)

- Shareholders Equity: What is left for the owners after all debts are paid (paid-in capital, retained earnings)

The Income Statement

The income statement shows whether the company made or lost money over a specific period of time, such as a quarter or a full year. Unlike the balance sheet, which is a snapshot, the income statement is a movie covering an entire reporting period.

It starts with total revenue at the top and subtracts all expenses to arrive at net income at the bottom, which is why it is sometimes called the profit and loss statement or P&L.

- Revenue: Total money earned from selling goods or services during the period

- Cost of Goods Sold: Direct costs of producing what was sold

- Operating Expenses: Indirect costs like salaries, rent, and marketing

- Net Income: The final profit or loss after all revenues and expenses

The Cash Flow Statement

The cash flow statement tracks the actual movement of cash into and out of the business during a period. This matters enormously because a company can show a profit on its income statement and still run out of cash. Many profitable businesses have failed because of poor cash management.

It is divided into three sections that cover every major source and use of cash.

- Operating Activities: Cash from the core business (collecting from customers, paying suppliers, wages)

- Investing Activities: Cash from buying or selling assets (equipment, buildings, investments)

- Financing Activities: Cash from borrowing, repaying debt, issuing stock, or paying dividends

Statement of Shareholders Equity

This statement explains how and why the ownership value of the company changed during the reporting period. It connects the balance sheets of two consecutive periods by showing what happened to equity in between.

Shareholders equity increases when the company earns profits (which add to retained earnings) or issues new shares. It decreases when the company pays dividends, buys back its own stock, or reports a loss.

- Opening Balance: Equity at the start of the period from the prior balance sheet

- Net Income or Loss: Profit or loss from the income statement added or subtracted

- Dividends Paid: Cash returned to shareholders reduces retained earnings

- Closing Balance: Equity at the end of the period, matching the new balance sheet

These four statements are not independent documents. They are deeply interconnected. Net income from the income statement flows into the statement of shareholders equity, which feeds into the closing equity balance on the balance sheet. The change in cash on the cash flow statement must match the change in the cash line on the balance sheet. When a company's four statements link correctly, it is strong evidence that the numbers are internally consistent and correctly prepared.

🌐 GAAP vs. IFRS: The Global Difference

While the United States uses GAAP, more than 140 other countries use a different framework called International Financial Reporting Standards (IFRS), which is developed by the International Accounting Standards Board (IASB), based in London.

This creates an important challenge for international investors and multinational companies. A German company's financial statements prepared under IFRS and an American company's statements prepared under GAAP are measuring similar things, but not always in the same way. Direct comparison requires careful adjustment.

| Topic | U.S. GAAP | IFRS | Difference Level |

|---|---|---|---|

| Overall Approach | Rules-Based | Principles-Based | Significant |

| Inventory Methods | FIFO, LIFO, and Weighted Average all allowed | FIFO and Weighted Average only. LIFO is prohibited. | Major |

| Research and Development Costs | Both research and development are expensed as incurred | Research expensed; certain development costs can be capitalized as an asset | Major |

| Asset Revaluation | Historical cost model. Assets generally cannot be written up above cost. | Revaluation model allowed. Assets can be written up to fair value. | Major |

| Intangible Assets | Only recognized if acquired in a business transaction | Can recognize internally generated intangibles if specific criteria are met | Significant |

| Revenue Recognition | ASC 606 five-step model | IFRS 15 five-step model (substantially converged) | Similar |

| Lease Accounting | ASC 842: most leases on balance sheet | IFRS 16: most leases on balance sheet (broadly similar) | Similar |

| Financial Statement Format | Specific formats are prescribed in detail | More flexibility in presentation format | Moderate |

| Extraordinary Items | Eliminated as a category (ASU 2015-01) | Also eliminated under IFRS | Same |

LIFO (Last-In, First-Out) is the single biggest practical difference between GAAP and IFRS. Under LIFO, companies assume the most recently purchased inventory is sold first. During periods of rising prices, this means higher costs are matched against revenue, resulting in lower reported profits and lower tax bills. Many U.S. companies use LIFO precisely for this tax benefit. Because IFRS prohibits LIFO entirely, a U.S. company switching to IFRS would see its reported profits and tax obligations change significantly.

👥 Who Must Follow GAAP?

The short answer is: all publicly traded companies in the United States must follow GAAP. But the complete picture is more nuanced, and understanding the full scope of who GAAP applies to matters if you are a business owner, investor, or accounting student.

| Entity Type | GAAP Required? | Enforcer | Notes |

|---|---|---|---|

| Publicly traded companies (NYSE, NASDAQ) | Yes, Mandatory | SEC | Must file 10-K and 10-Q reports with the SEC using GAAP. Non-compliance is a federal violation. |

| Private companies seeking bank financing | Often Required by Lenders | Lenders / Covenants | Banks and private lenders frequently require GAAP-compliant financial statements as a loan condition. |

| Private companies planning to go public | Yes, Required | SEC (IPO process) | Must adopt GAAP during the IPO preparation process before filing with the SEC. |

| Small private businesses (sole traders, LLCs) | No, Optional | N/A | No legal requirement to follow GAAP. However, using GAAP improves credibility and investor readiness. |

| State and local governments | GASB Standards | GASB | Follow Government GAAP set by GASB, which differs from FASB GAAP in several important ways. |

| Federal government agencies | FASAB Standards | FASAB | Use Federal GAAP developed by the Federal Accounting Standards Advisory Board. |

| Nonprofit organizations | FASB GAAP Applies | FASB / IRS | Nonprofits follow FASB GAAP but use different financial statement formats and terminology than for-profit entities. |

📈 GAAP Updates and Trends in 2026

GAAP is not static. FASB regularly issues Accounting Standards Updates (ASUs) to address new economic realities, close loopholes, improve disclosure quality, and respond to feedback from preparers and investors. Here are the most significant developments shaping GAAP in 2025 and 2026.

Segment Reporting Overhaul (ASU 2023-07)

One of the most significant recent changes to GAAP, effective for annual periods beginning after December 15, 2023, is the update to segment reporting under ASC 280. Companies must now disclose significant segment expenses and other segment items on an annual and interim basis. This gives investors much better visibility into how large, diversified companies make their money and where their costs actually lie. Before this update, companies could disclose very limited information at the segment level, making it difficult for investors to understand the economics of individual business units.

Crypto Asset Accounting (ASU 2023-08)

For fiscal years beginning after December 15, 2024, companies holding certain qualifying crypto assets (including Bitcoin and Ether) must measure them at fair value and recognize changes in fair value in net income each period. This is a dramatic departure from the previous practice of treating crypto as an indefinite-lived intangible asset measured at cost, which allowed large unrealized losses to accumulate invisibly. The new standard makes crypto holdings much more transparent but also introduces significant volatility into reported income for companies holding large crypto positions.

Income Tax Disclosures (ASU 2023-09)

Effective for fiscal years beginning after December 15, 2024, this update significantly expands what companies must disclose about their income taxes. Companies must now provide a detailed breakdown of the rate reconciliation and disclose income taxes paid disaggregated by jurisdiction. For investors and policymakers concerned about corporate tax planning and cross-border profit shifting, this represents a meaningful improvement in transparency.

The Ongoing Conversation About GAAP and IFRS

Despite decades of convergence efforts, the United States has shown no signs of abandoning GAAP in favour of IFRS. The SEC periodically revisits this question and has consistently concluded that the domestic benefits of GAAP, including the deep body of interpretive guidance, the enforcement infrastructure, and the familiarity of U.S. investors and preparers, outweigh the global harmonization benefits of IFRS adoption. As of 2026, GAAP and IFRS continue to coexist as parallel systems, with ongoing efforts to align them on new standards where possible.

✦ Why GAAP Matters to Everyone

GAAP might sound like a topic only for accountants and auditors, but its effects reach into every corner of the economy. When a teacher's pension fund invests in a company's stock, it is relying on GAAP-compliant financial statements to make that decision. When a bank decides whether to lend money to a business, it uses GAAP financial statements to evaluate risk. When a government regulator investigates a potential fraud, GAAP provides the benchmark for what the numbers should have looked like.

The history of financial scandals, from the accounting frauds of Enron and WorldCom in the early 2000s to more recent reporting controversies, consistently shows what happens when the principles behind GAAP are violated. Investors lose savings. Employees lose jobs. Public trust in markets erodes. GAAP is not just bureaucratic paperwork. It is one of the foundational systems that keeps financial markets honest enough to function.

Understanding these principles, even at a basic level, makes you a more informed investor, a more effective business owner, and a more critical reader of the financial news that shapes the world around you.

- 1GAAP is the standardized accounting rulebook for U.S. companies, developed by FASB and enforced by the SEC for publicly traded entities. It exists to make financial information consistent, comparable, and trustworthy.

- 2The 10 core principles cover everything from basic honesty (sincerity) and stability (consistency) to caution (prudence) and completeness (materiality). Together they define what good accounting behavior looks like.

- 3Four financial statements (balance sheet, income statement, cash flow statement, and statement of shareholders equity) give a complete and interconnected picture of a company's financial health when prepared correctly under GAAP.

- 4GAAP and IFRS are not the same. The biggest practical differences involve inventory (LIFO is only allowed under GAAP), research and development costs, and asset revaluation. These differences can produce materially different profit figures for the same business.

- 5GAAP keeps evolving. The 2025-2026 updates on crypto asset fair value accounting and expanded income tax disclosures show that FASB continues to update the rules to keep pace with how businesses operate and what investors need to know.

❓ Frequently Asked Questions

References and Further Reading

- Financial Accounting Standards Board (FASB). (2024). FASB Accounting Standards Codification. The single authoritative source of U.S. GAAP for nongovernmental entities. asc.fasb.org

- FASB. (2023). Accounting Standards Update 2023-08: Accounting for and Disclosure of Crypto Assets. Financial Accounting Standards Board. Read at FASB.org

- FASB. (2023). Accounting Standards Update 2023-07: Segment Reporting (Topic 280). Financial Accounting Standards Board. Read at FASB.org

- FASB. (2023). Accounting Standards Update 2023-09: Income Taxes (Topic 740). Financial Accounting Standards Board. Read at FASB.org

- Securities and Exchange Commission (SEC). (2024). Financial Reporting Manual. U.S. Securities and Exchange Commission Division of Corporation Finance. sec.gov

- Kieso, D. E., Weygandt, J. J., & Warfield, T. D. (2022). Intermediate Accounting (17th ed.). John Wiley & Sons. ISBN: 978-1119503637

- Wild, J. J., Shaw, K. W., & Chiappetta, B. (2023). Principles of Accounting (27th ed.). McGraw Hill Education.

- International Financial Reporting Standards Foundation. (2024). IFRS Accounting Standards. IFRS Foundation. ifrs.org

- American Institute of CPAs (AICPA). (2024). U.S. GAAP vs. IFRS: The Basics. AICPA. aicpa.org

- Public Company Accounting Oversight Board (PCAOB). (2024). Auditing Standards. PCAOB. pcaobus.org

Nilambar is a research educator and knowledge advocate based in Nepal. He writes about economics, accounting, research methodology, and data literacy to make complex academic and professional topics genuinely accessible to students, educators, and curious minds everywhere. His mission is simple: knowledge shared freely is knowledge multiplied. More of his writing is available at nilambarkhanal.com.np.

Found This Guide Genuinely Useful?

Share it with a student, business owner, or investor who wants to understand how financial reporting actually works.

Post a Comment